Are you dreaming of owning your first home in California but feel like the down payment is an impossible mountain to climb? You aren't alone. With home prices in the Golden State reaching new heights, many hardworking families feel stuck in the "renter’s trap." But there is a solution that could change everything for you: the CalHFA voucher program, specifically the California Dream For All Shared Appreciation Loan.

At Maya Team Inc., we believe that everyone deserves a chance at homeownership. As your trusted educators and consultants, we want to help you navigate the complex world of state-funded assistance. Whether you are looking for a massive boost to your down payment or a smaller "gap" loan to cover closing costs, knowing how these programs work is the first step toward holding those keys in your hand.

Here is the short answer: The CalHFA "voucher" is part of a lottery-based system where eligible first-generation, first-time homebuyers can receive up to twenty percent of their home’s purchase price (up to one hundred fifty thousand dollars) to use toward a down payment or closing costs. However, you must register during a specific window: for 2026, that is February twenty-fourth through March sixteenth: to even be considered.

Let’s dive into the ten most important things you need to know about CalHFA vouchers and down payment assistance right now.

1. What Exactly is the CalHFA "Voucher"?

When people talk about a "CalHFA voucher" in 2026, they are usually referring to the California Dream For All (DFA) Shared Appreciation Loan. This isn't a traditional coupon you take to the grocery store. Instead, it is a reservation of funds. Because the state has a limited pool of money: approximately two hundred million dollars to three hundred million dollars for the current cycle: they use a randomized drawing to select who gets the help.

If you are selected in the lottery, you receive a voucher. This voucher proves to your lender and to home sellers that you have the state’s backing for a significant down payment. This can make your offer much stronger in a competitive market.

2. The "First-Generation" Requirement is Critical

For the Dream For All voucher, being a first-time homebuyer isn't enough. At least one borrower on the loan must also be a first-generation homebuyer.

What does that mean? Generally, it means your parents do not currently own a home in the United States. If you grew up in a home that your parents owned but they sold it years ago, you might still qualify, but the specific rule is that they cannot have an ownership interest in a home at the time you apply. This program is specifically designed to help families who haven't had the benefit of generational wealth through real estate.

3. How Much Money Can You Actually Get?

This is the most exciting part for many buyers. The Dream For All program offers up to twenty percent of the home’s purchase price or appraised value, whichever is less. However, there is a hard cap of one hundred fifty thousand dollars.

For example, if you are buying a home for five hundred thousand dollars, twenty percent would be one hundred thousand dollars. That is a massive head start that can lower your monthly mortgage payment significantly because you are borrowing less from the bank.

4. It Is a "Shared Appreciation" Loan, Not a Grant

It is vital to understand that this money is not a "gift" or a "grant" that never has to be repaid. It is a loan with zero percent interest and no monthly payments, but it comes with a "shared appreciation" clause.

When you eventually sell the home, refinance the mortgage, or pay off the first loan, you must repay the original amount you borrowed plus a percentage of any "appreciation" (the increase in value) your home has gained. For most buyers, the state takes twenty percent of the profit you made on the home’s value. If the home didn't go up in value, you just owe the original amount back.

5. There is a Very Strict Registration Window

You cannot apply for a voucher whenever you want. For the 2026 cycle, the registration portal opens on February twenty-fourth, 2026, and closes promptly at five o'clock in the evening on March sixteenth, 2026.

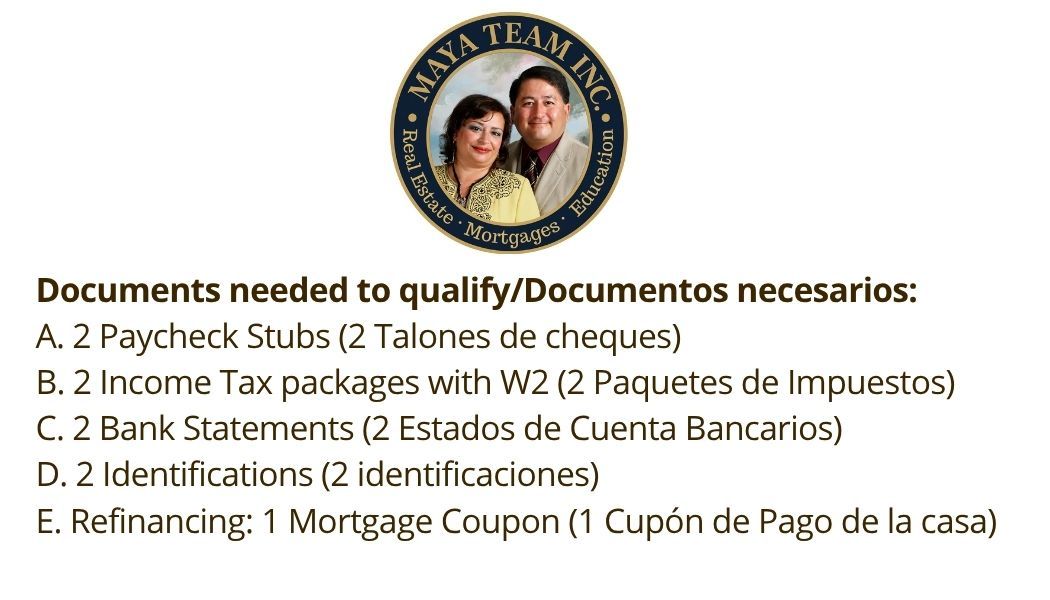

If you miss this window, you cannot get a voucher for this round. This is why we tell all our clients at Maya Team Inc. to get their documents ready months in advance. You need a "Pre-Registration Letter" from a CalHFA-approved lender like Rony Velasquez to even enter the lottery.

6. Income Limits Apply by County

Not everyone qualifies for these programs. CalHFA sets income limits based on the county where you are buying the home. These limits are designed to ensure the money goes to low-to-moderate-income families.

For example, the income limit in Los Angeles County might be different than the limit in Riverside or San Bernardino. If your household earns more than the limit for that specific county, you won't be eligible for the Dream For All voucher, though you might still qualify for other programs.

7. The "MyHome" Backup Plan

What happens if you aren't lucky enough to win the lottery? Don't give up! CalHFA has a permanent program called MyHome Assistance.

Unlike the voucher program, MyHome is available year-round and isn't a lottery. It provides a smaller amount of help: usually three percent or three point five percent of the purchase price. While it isn't as large as the twenty percent offered by Dream For All, it can still cover your entire down payment for an FHA loan (which requires three point five percent down).

8. Credit Score and Debt-to-Income (DTI) Matters

Even if you have a voucher, you still have to "qualify" for the actual mortgage. Most CalHFA programs require a minimum credit score (often around six hundred sixty to six hundred eighty).

Additionally, lenders look at your Debt-to-Income (DTI) ratio. This is the percentage of your monthly gross income that goes toward paying debts (like car loans, student loans, and your new mortgage). Usually, you want this to be under forty-five to fifty percent. If you have too much debt, you might not be able to use the full twenty percent voucher because you can't afford the remaining eighty percent of the loan.

9. You Must Complete Homebuyer Education

CalHFA requires all borrowers to complete a homebuyer education counseling course. This is a great way to learn about the responsibilities of being a homeowner, from maintenance to property taxes. There is usually a small fee (around ninety-nine dollars) for the online course, and you must receive a certificate of completion to finalize your loan.

10. You Must Work with a CalHFA-Approved Lender

You cannot just walk into any big-name bank and ask for a CalHFA voucher. You must work with a CalHFA-approved lender who is trained in these specific programs.

At Maya Team Inc., our Mortgage Loan Originator, Rony Velasquez, specializes in these California-specific programs. We help you gather your tax returns, pay stubs, and bank statements to ensure your application is "lottery-ready." Having a professional who understands the nuances of FHA and Conventional CalHFA loans is the difference between an approved voucher and a denied application.

Are You Ready to Apply?

The journey to homeownership can feel overwhelming, but you don't have to do it alone. Whether you are a first-time homebuyer in Los Angeles, Orange County, or the Inland Empire, the CalHFA programs are one of the most powerful tools available to help you build wealth for your family.

Remember, the Dream For All lottery is a rare opportunity. If you meet the first-generation and first-time buyer requirements, you owe it to yourself to try. And if the lottery doesn't go your way, we have dozens of other loan products: from FHA to Conventional and MyHome assistance: that can still get you into a home with very little money out of pocket.

Do you have questions about the first-generation requirement or the 2026 income limits? Write a comment below, and let's start the conversation! We would love to hear your thoughts or help clarify any part of the process.

Contact Maya Team Inc. Today

If you are ready to see if you qualify for a CalHFA voucher or any other down payment assistance program, reach out to us. We are here to serve as your professional consultants and guide you home.

Rony Velasquez

Real Estate and Mortgage Broker

Mortgage Loan Originator (MLO) & Realtor®

Mobile: 562-762-9634

Email: mayateaminc@gmail.com

Mona Bottros

Realtor® and Office Manager

Visit our website for more resources: https://nas.io/mayateaminc