Buying your first home in California can feel like trying to climb a mountain in flip-flops. With home prices reaching new heights every year, the dream of homeownership often feels just out of reach. That is why everyone is talking about the CalHFA Dream for All Shared Appreciation Loan.

But with any big financial program, there is always a lot of chatter. Is it a "trap"? Is it "bad"? Or is it the bridge you’ve been waiting for? We are here to clear the air. As your dedicated team at Maya Team Inc., Rony Velasquez and Mona Bottros believe in giving you the straight facts so you can make a choice that fits your family's future.

The Short Answer: Is It Bad?

The CalHFA Shared Appreciation Loan is not "bad," but it is a trade-off. It gives you a massive amount of cash today: up to twenty percent of the purchase price or one hundred fifty thousand dollars: to help you buy a home. In return, you agree to share a portion of the home’s future growth (appreciation) with the state when you sell or refinance.

If you need the help to get in the door today, it’s a lifesaver. If you already have a big down payment saved, it might not be the best move.

What is the CalHFA Shared Appreciation Loan?

The "Dream for All" program is a down payment assistance loan designed specifically for first-time homebuyers in California. Unlike a traditional loan where you pay back the principal plus interest every month, this is a second mortgage that requires no monthly payments.

How the "Shared Appreciation" part works:

When you eventually sell your home or refinance your mortgage, you have to pay back:

- The original amount you borrowed (the principal).

- A share of the home's appreciation. For most buyers, this is twenty percent of the increase in the home’s value.

For example, if you buy a home for five hundred thousand dollars and sell it years later for seven hundred thousand dollars, you would owe the original assistance plus twenty percent of that two hundred thousand dollar gain.

The Pros: Why First-Time Buyers Love It

There are some very clear reasons why this program is so popular. It tackles the biggest hurdle in real estate: the upfront cash.

- Massive Down Payment Support: Getting up to twenty percent down (maxing out at one hundred fifty thousand dollars) is a game-changer. It can turn a "no" from a lender into a "yes."

- Lower Monthly Payments: Because you are putting twenty percent down, your "first" mortgage is smaller. This means your monthly mortgage payment is much lower than if you only put three percent or five percent down.

- No Monthly Interest: You aren't paying interest on this assistance every month. The "cost" is deferred until you move or refinance.

- No Private Mortgage Insurance (PMI): Putting twenty percent down typically allows you to avoid PMI, which can save you two hundred dollars to five hundred dollars every single month.

The Cons: What You Need to Watch Out For

It’s not free money. You are essentially taking on a business partner (the State of California) in your home.

- Giving Up Future Wealth: If your home value skyrockets, the amount you pay back could be much higher than a standard interest rate would have been. You are trading future equity for present-day access.

- Zero Initial Equity: Because the down payment is a loan, you start with zero true equity of your own. If the market dips shortly after you buy, you could owe more than the home is worth.

- Refinancing Restrictions: If you want to refinance later to get a lower rate, you might have to pay back the entire Shared Appreciation loan at that time, which can be a huge financial hurdle.

Understanding the Technical Jargon

Before you apply, it is important to understand a few terms that the "underwriting" team (the people who approve your loan) will be looking at:

- FICO Score: This is your credit score. For most CalHFA programs, you generally need a score of at least six hundred sixty or six hundred eighty, depending on your income level.

- DTI (Debt-to-Income Ratio): This is the percentage of your monthly income that goes toward paying debts. To qualify, lenders usually want to see this below forty-five percent or fifty percent.

- Underwriting: This is the process where the bank verifies your income, assets, and credit to make sure you can afford the home.

Who Is This Program For?

This loan is specifically targeted at first-generation homebuyers. This means your parents do not currently own a home in the United States. If you are the first in your family to plant roots and build wealth through real estate, this program was built with you in mind.

It is also great for those who have a solid income to handle a monthly payment but haven't been able to save the sixty thousand dollars or one hundred thousand dollars needed for a down payment in California’s expensive markets.

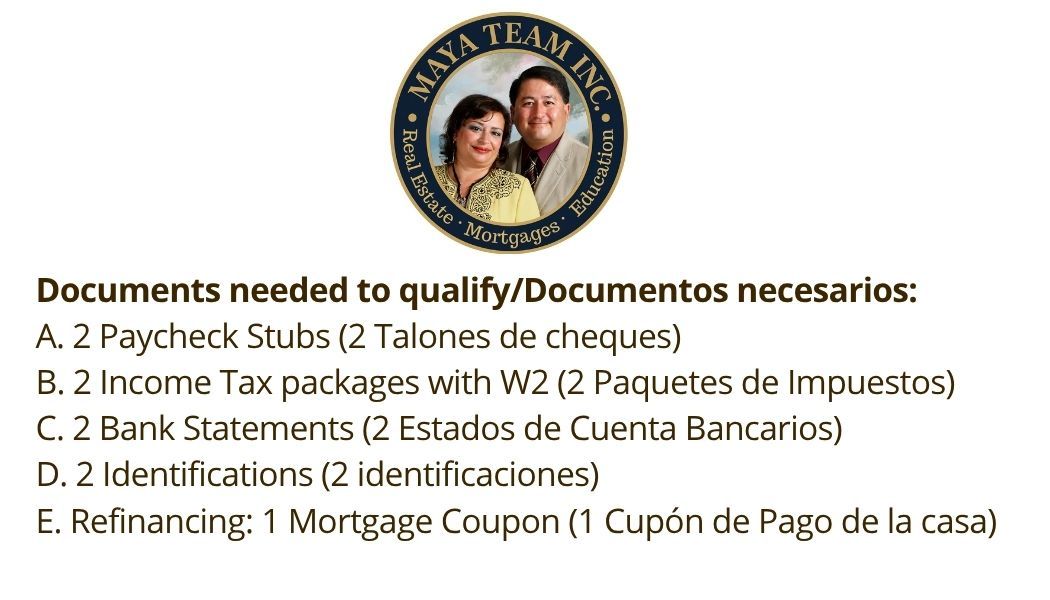

Your First-Time Buyer Checklist

If you are thinking about jumping into the "Dream for All" lottery or any CalHFA program, here is what you need to have ready:

- Two paycheck stubs (your most recent ones).

- Two years of tax packages (including W2s).

- Two months of bank statements (all pages).

- Two forms of identification (Driver’s license, Passport, etc.).

- A certificate of completion for a state-approved homebuyer education course.

How to Get Started

The CalHFA Shared Appreciation Loan often operates on a "voucher" or lottery system because it is so popular. You cannot just apply anytime; you have to be ready when the window opens.

Working with an experienced Mortgage Loan Originator (MLO) like Rony Velasquez is the best way to ensure your paperwork is perfect before the deadline. We help you look at the numbers: the "what ifs": so you aren't surprised five years from now.

Let’s Make Your Move

Is the Shared Appreciation loan right for you? There is only one way to find out for sure: let’s run your specific numbers. At Maya Team Inc., we don’t just sell houses; we help you build a financial foundation.

Contact us today to start your journey:

- Visit our community: nas.io/mayateaminc

- Call or Text us: Reach out to Rony or Mona directly to schedule a free consultation.

- Follow us: Stay updated on the latest CalHFA news and real estate tips by joining our online group.

We look forward to helping you unlock the door to your first home!

Rony Velasquez

Real Estate and Mortgage Broker | Realtor® | Mortgage Loan Originator (MLO)

Mona Bottros

Realtor® and Office Manager